by: Barry Friends | Bob Goldin

August 17, 2017

Five publicly traded distributors – Sysco, US Foods, Performance Food Group (PFG), Chef’s Warehouse and United Natural Foods (UNFI) – do an estimated $85 billion in U.S. foodservice volume (UNFI is primarily a distributor to the natural/organic retail channel but does several hundred million dollars in foodservice). Their combined volume represents almost 30% of the market. They sell to hundreds of thousands of foodservice customers of all types and, therefore, provide a comprehensive look at broad market trends.

Five publicly traded distributors – Sysco, US Foods, Performance Food Group (PFG), Chef’s Warehouse and United Natural Foods (UNFI) – do an estimated $85 billion in U.S. foodservice volume (UNFI is primarily a distributor to the natural/organic retail channel but does several hundred million dollars in foodservice). Their combined volume represents almost 30% of the market. They sell to hundreds of thousands of foodservice customers of all types and, therefore, provide a comprehensive look at broad market trends.

Over the past few weeks, the above companies have reported their latest quarterly results (in a few instances, the quarter contained a 14th week; Pentallect adjusted the numbers to reflect a 13-week quarter that is comparable to the prior year). The results reflect solid and improving performance; they also strongly suggest that the industry is growing despite softness in the certain segments and regions.

Some highlights include:

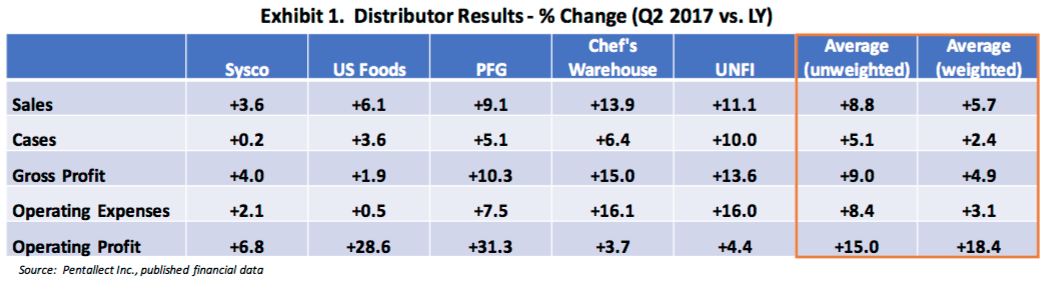

- As shown in Exhibit 1, company volume and profit trends are positive. For Sysco, US Foods and PFG, profit growth is outpacing volume growth due to volume gains, mix improvements and operating expense control.

- After a long hiatus, food cost inflation has returned, most notably in produce, poultry, cheeses and seafood. We are estimating inflation is in the 3 – 4% range. As distributors pass along their cost increases, inflation will add pressure on operators who are already grappling with sharply higher labor costs.

- Operator pain notwithstanding, moderate inflation is a distributor’s “friend”, enabling predictable margin gains when re-valuing inventory on a LIFO accounting basis.

- For Sysco, US Foods and PFG, case volume growth to independent operators averages 5%, which exceeds their overall case volume growth of 3%. This is a sure sign that independents are doing well (contrary to what some industry analysts report).

- Results show that Sysco and US Foods have fully recovered from their 2013-2015 failed merger attempt and are regaining business lost during that difficult period, especially on US Foods’ part.

- On investor calls and in published reports, Sysco, US Foods and PFG each stated that their private brand sales are outpacing their overall sales. This trend is certainly improving their profitability as distributor brands have superior margins.

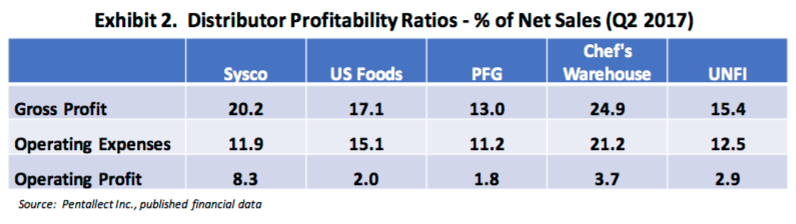

- Exhibit 2 illustrates how customer mix, product portfolio and size affect profitability.

Exhibit 1 Notes:

1. Data are for latest quarter, 2017, and exclude one-time restructuring charges.

2. UNFI data are for all channels. Foodservice is less than 10% of total.

3. Sysco reports case volume for independents (“local”) are +2.7%; for USF, the comparable number is +4.7% and for PFG it is +7.0%.

While the political climate is troubling, we are guardedly optimistic that the evident industry momentum revealed by the distributors’ positive reports will continue for the balance of the year, if not longer.