May 17, 2021

To mitigate the economic ravages of the COVID-19 pandemic, foodservice distributors implemented a variety of critical initiatives with a true sense of urgency. To varying degrees, they engaged in serious cost cutting, product and customer mix improvement, operational efficiency enhancements, and financial engineering/restructuring¹ that enabled them to reduce their break-even, bolster their liquidity, and improve their cash flow. Despite a case volume reduction in the 25% range over the past year, it appears that structural damage has been largely averted; with the severity of the pandemic ebbing (due in large part to our country’s success with vaccinations) and foodservice beginning to recover, distributors – while certainly “bruised and battered” – should be able to continue to provide the operator community with excellent service and support.

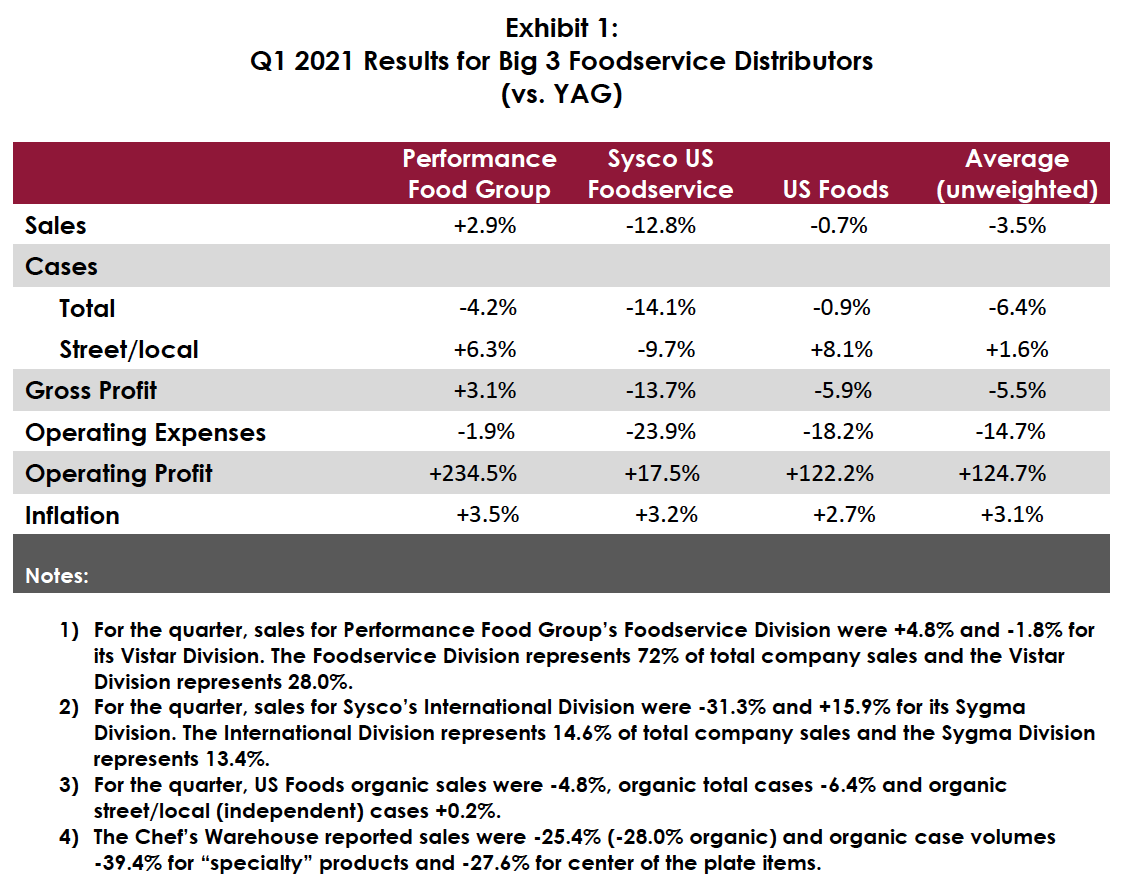

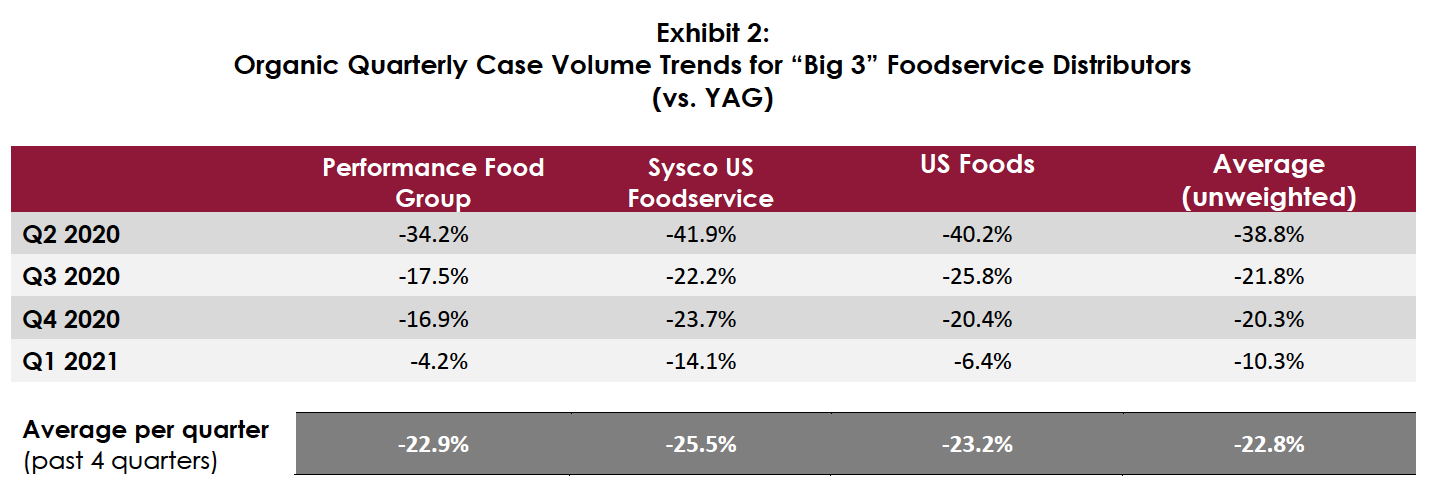

As shown in Exhibits 1 and 2 below, the most recent results for the “Big 3” foodservice distributors illustrate some favorable trends, most notably a marked sequential improvement in case volumes (especially with independents), and major success in operating expense reduction. Organic case volume was -10.3% for Q1 2021 vs. -20.3% for Q4 2020. However, significant margin pressures and challenges continue to exist and in many cases are accelerating. These include but are by no means limited to the following:

- Increased and increasing product and labor costs, including driver and warehouse personnel shortages. As they were pre-pandemic, driver shortages appear to be especially dire.

- Supply chain bottlenecks, many of which are compounded by labor shortages and are affecting distributors’ ability to service their operator customers.

- Slow “recovery rates” in certain high-volume geo-markets (including, for Sysco, the Eurozone) and segments.

- Ongoing access and occupancy restrictions (although they are easing).

- A shrunken independent restaurant operator universe (although Pentallect does believe that there will be an influx of new entrants over the next 12 – 36 months).

- A pandemic-accelerated consumer stomach share shift from full-service (mostly independent) to quick-service (mostly chain) outlets whose scale and supply chain sophistication translate to markedly lower distributor margins (note Sygma vs. Sysco Broadline YOY margin comparatives).

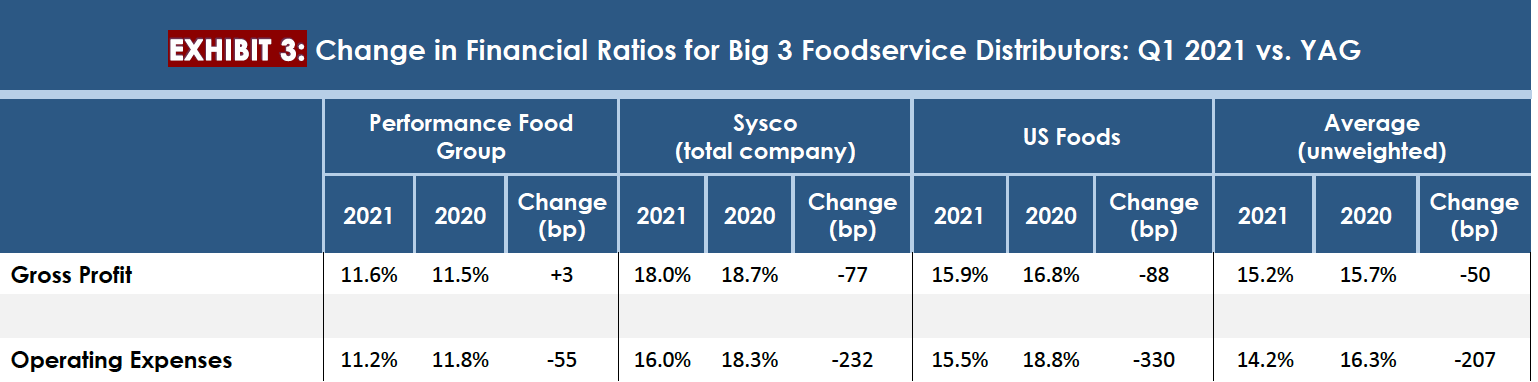

Compared to a year ago, the Big 3 have experienced an average 50 basis point (bp) decline in gross profit margin but have dramatically improved their cash flow from operations and reduced their operating expense margin by 207 basis points² – a truly impressive accomplishment under very trying circumstances.

Executives from the Big 3 express a lot of optimism about the scope and timing of the foodservice rebound, and we generally concur with them. They are investing in people, processes, and inventory to ready themselves for a strong second half of 2021 and beyond. They are “leaner and meaner” companies and, while they do face many strong headwinds, they should be in an excellent position to benefit by an improving demand scenario.

¹Some were able to avail themselves of government support programs such as PPP loans.

² A reduction in bad debt allowances favorably impacted operating expenses.

By: Bob Goldin | Barry Friends

.