![]()

By: Bob Goldin | Rob Veidenheimer

January 27, 2020

Food and beverage manufacturer sales were $860 billion in 2019. Of this total, $245 billion (29%) was private label¹. In retail, private label share is 21%; in foodservice it is 45%.

Food and beverage manufacturer sales were $860 billion in 2019. Of this total, $245 billion (29%) was private label¹. In retail, private label share is 21%; in foodservice it is 45%.

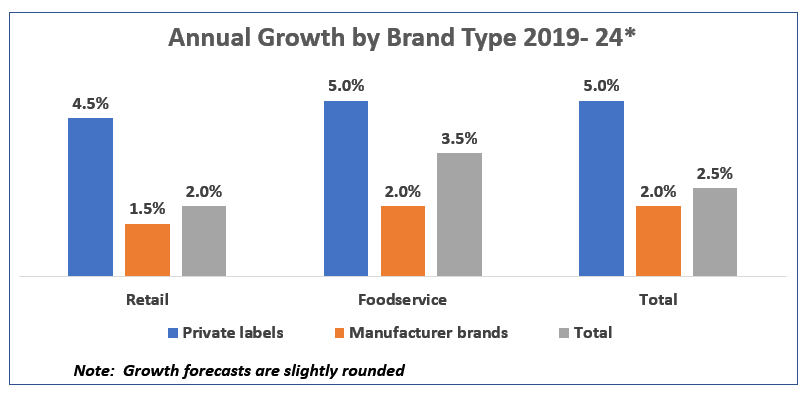

Over the past decade, private label has grown consistently and well in excess of manufacturer brands² in both retail³ and foodservice markets. Many manufacturers under-invested in their own (big) brands and/or shifted focus to much smaller “on trend” brands which they acquired or developed at great expense. This, coupled with a major power shift toward “mega” customers, enabled private labels to gain valuable foundational penetration from which they have successfully expanded.

The relative growth of private label will accelerate as private label customers of all types improve and contemporize their offerings, broaden their category focus, enhance their marketing and continue to gain consumer loyalty based on product quality, uniqueness and value. Private label performance will be further fueled by the rapid growth of companies like Aldi, Trader Joe’s, Wegman’s, Costco, Sysco and many others, including a number of nontraditional retailers, that are fully committed to and extremely effective at private label development. We forecast that private label will grow at approximately 5.0% annually over the next five years, with comparable growth across both the foodservice and retail channels, versus 2.0% for manufacturer brands. By 2024, private label share will be 32%.

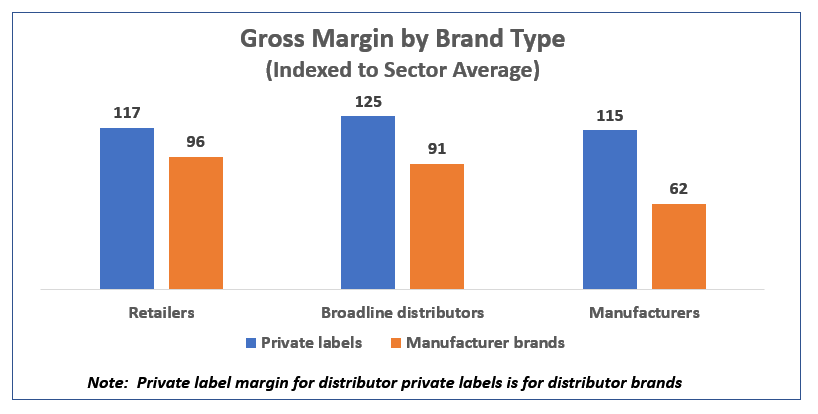

The growth of private label has major implications on the food and beverage industry profit pool. For retailers and broadline distributors, private label is a boon – it is 300 – 500 basis points more profitable than manufacturer brands. The unquestionably favorable economics of private label is a major reason for why these companies focus so intently on it. For most manufacturers, however, private label is significantly lower margin (even though the spread is narrowing a bit due to a ramp-up of costly A & P on manufacturer brands). As manufacturer sales grow, margin contraction will occur as lower margin private label sales become a more significant part of the mix.

Private label poses a real challenge for branded manufacturers. It is a large, dynamic part of the business that is increasingly resonating with trade customers and consumers and may be considered “too big to ignore.” However, it is typically much lower margin and can be costly to serve due to a variety of supply chain and trade support issues. Further, many branded manufacturers lack the low-cost manufacturing position required to profitably participate in the category. In our view, the most prudent course of action for branded manufacturers is to “play to their strengths” (namely national brands) which necessitates greater and more creative investment in core profitable brands. Manufacturers must also quantify the true cost-to-serve for their manufacturer versus private label businesses in order to clarify strategic priorities and refine executional practices. At the same time, pursuing a lower cost position is an increasing imperative.

¹Private label includes retailer (store), distributor/wholesaler and chain restaurant brands. Sales estimates exclude alcoholic beverages.

²Manufacturer brands include packer labels.

³Retail includes nontraditional channels like club stores, online, limited assortment stores, etc.

In mid-February, Pentallect will be issuing a comprehensive report on food and beverage brand dynamics, entitled: