By: Rob Veidenheimer | Bob Goldin

October 2, 2019

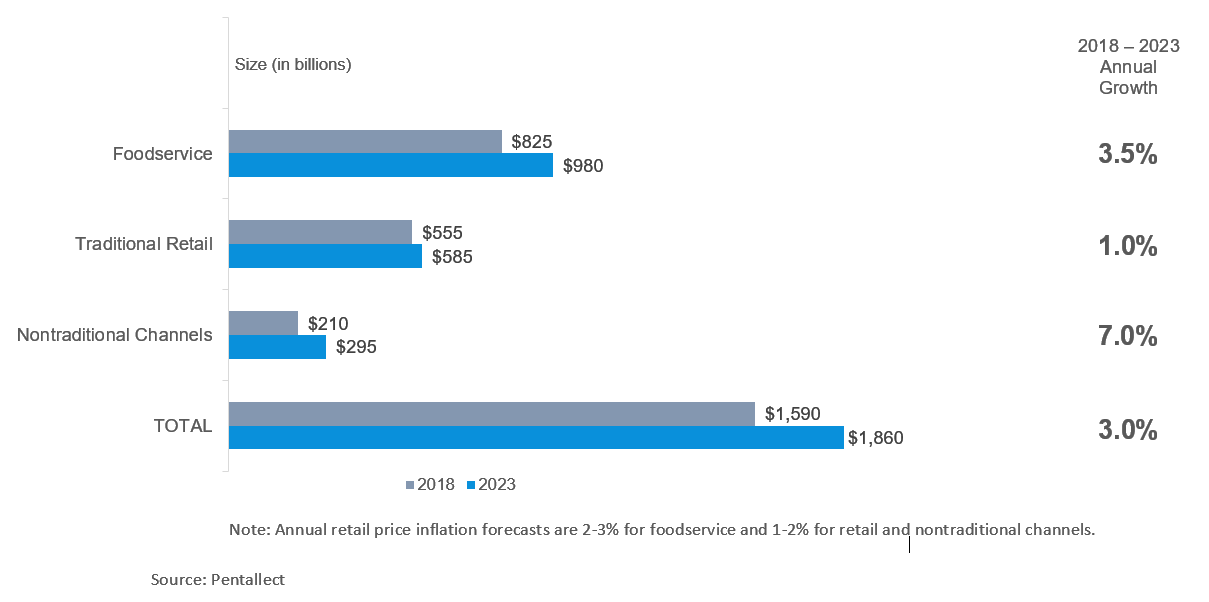

Broadly speaking, the $1.6 trillion U.S. food and beverage industry is composed of two major segments: Retail and Foodservice. Within these segments, major sub-segments are thoroughly measured by tracking services such as IRI, AC Nielsen, Spins, Technomic, the National Restaurant Association and the government.

Broadly speaking, the $1.6 trillion U.S. food and beverage industry is composed of two major segments: Retail and Foodservice. Within these segments, major sub-segments are thoroughly measured by tracking services such as IRI, AC Nielsen, Spins, Technomic, the National Restaurant Association and the government.

However, over the recent past several nontraditional, primarily retail, channels have emerged and/or solidified their positions, and are poised for accelerated growth at the expense of traditional channels. These nontraditional channels “fly under the radar screen” insofar as they are not systematically measured by established services.

Pentallect conducted comprehensive research and analysis into 10 nontraditional channels, including obtaining insights from over 1,000 consumers, and the findings are documented in our new report: Nontraditional Food Channels: A Key Industry Growth Driver, an update of a major report we did on the topic in 2017. The nontraditional channels that were researched include: club stores, community supported agriculture (CSA), ethnic/neighborhood stores (e.g., bodegas), farmers markets, food trucks, limited assortment stores, meal kits/home delivered meals, online, specialty stores (e.g., bakeries, butchers, etc.) and Trader Joe’s.

Key Findings

A summary of primary insights from the research include:

- Nontraditional channels will account for almost one-third of all food industry growth through 2023, accounting for an incremental $85 billion in consumer spending.

- Traditional Retail will be negatively impacted the most by nontraditional channel growth.

- Frequency of use is high among users and overall market penetration remains relatively low; indicating significant upside potential.

- The nontraditional channels, collectively, will grow at more than double the rate of the overall food industry as two-thirds of consumers plan to use nontraditional channels the same or more, or will try them.

Implications

As food industry structure shifts, new growth pockets emerge and traditional sources of volume and profit stagnate or contract, we advise our clients to:

- Reevaluate channel priorities to identify the greatest growth opportunities for their unique value proposition, which will likely be different from current channel, segment and customer priorities.

- Assess resource allocations (structure and spending) between traditional and nontraditional channels to support revised priorities, position the organization for success and achieve an acceptable ROI.

- Ensure that supporting capabilities and innovation efforts evolve to meet the changing requirements for success.

Learn more about/order the Nontraditional Food Channels: A Key Industry Growth Driver report

Please contact us if you would like to discuss Nontraditional Channels and the implications for your business in greater detail.