November 15, 2021

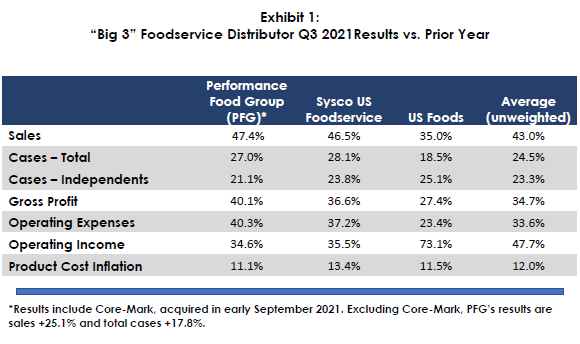

The collectively impressive third quarter 2021 results of the “Big 3” foodservice distributors – Performance Food Group (PFG), Sysco US Foodservice and US Foods – are a clear indication of a sequentially improving market, customer wins, improved customer and product mix, M&A activity, and success in passing along unprecedented product and labor cost increases.

The “Big 3” reported product cost inflation – paced by proteins and disposables – of 12%; Pentallect estimates that their labor costs, primarily for drivers and selectors, were +10 – 20%, with further increases likely. These cost increases are anomalous – historically, product and labor cost increases averaged 1 – 2% each per year. We anticipate that a good portion of the cost increases will be permanent in nature, although we do expect to see customer resistance at some point. Depending upon how distributors pass along inflation, it can be margin dollar accretive and margin percent dilutive. We suspect this is the case with the “Big 3” as they have all experienced material margin percentage declines vs. last year.

In this supply challenged environment, the “Big 3” are effectively leveraging their size, scale, resources, and strategic investments to achieve “above market” sales and case volume growth and greatly improved profitability. Customers of all type, including major chains, are prioritizing reliable and secure supply sources, and the “Big 3” have invested heavily in inventory, processes and people to enable them to provide competitively superior service to “customers that matter” to them. While the “Big 3” are experiencing ongoing and serious product shortages and other supply chain disruptions like others in foodservice and other industries, their supply chains are relatively strong and resilient. We expect the customer “flight to safety” will continue to benefit the “Big 3” and selected other uniquely advantaged distributors; it is also likely to benefit many established brands.

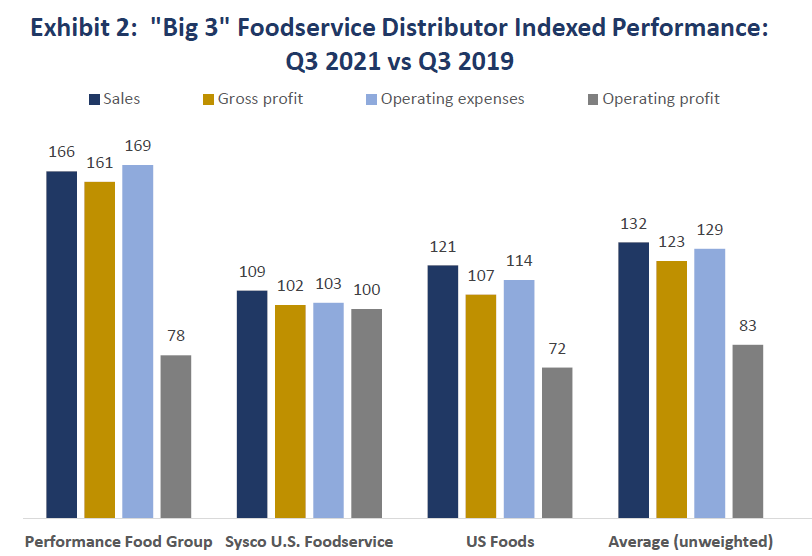

As shown below, third quarter 2021 sales¹ of the “Big 3” are well ahead (32% on average²) of what they were in the comparable 2019 period, fueled in large part by US Foods and PFG’s acquisitions. We estimate the foodservice industry is -7.5% (indexed sales of around 92.5), so this implies that the “Big 3” have gained 6 – 7 share points. This represents a very significant structural development with major implications to all industry participants.

Sysco’s $10+ billion International Division increased sales by 33.8%, an encouraging sign that the effects of the pandemic are easing in many major overseas markets. We expect the international recovery to accelerate in the upcoming months as travel and other restrictions are lifted.

It appears that the distribution industry is in a consolidation phase as both strategic and financial buyers are highly interested in the space. We fully expect that additional M & A activity will take place in the near future.

¹Includes acquisitions and PFG’s Eby Brown and Core-Mark businesses, and exclude Sysco’s Sygma Division

²+19.8% on a weighted basis