![]()

By: Bob Goldin | Barry Friends

August 17, 2020

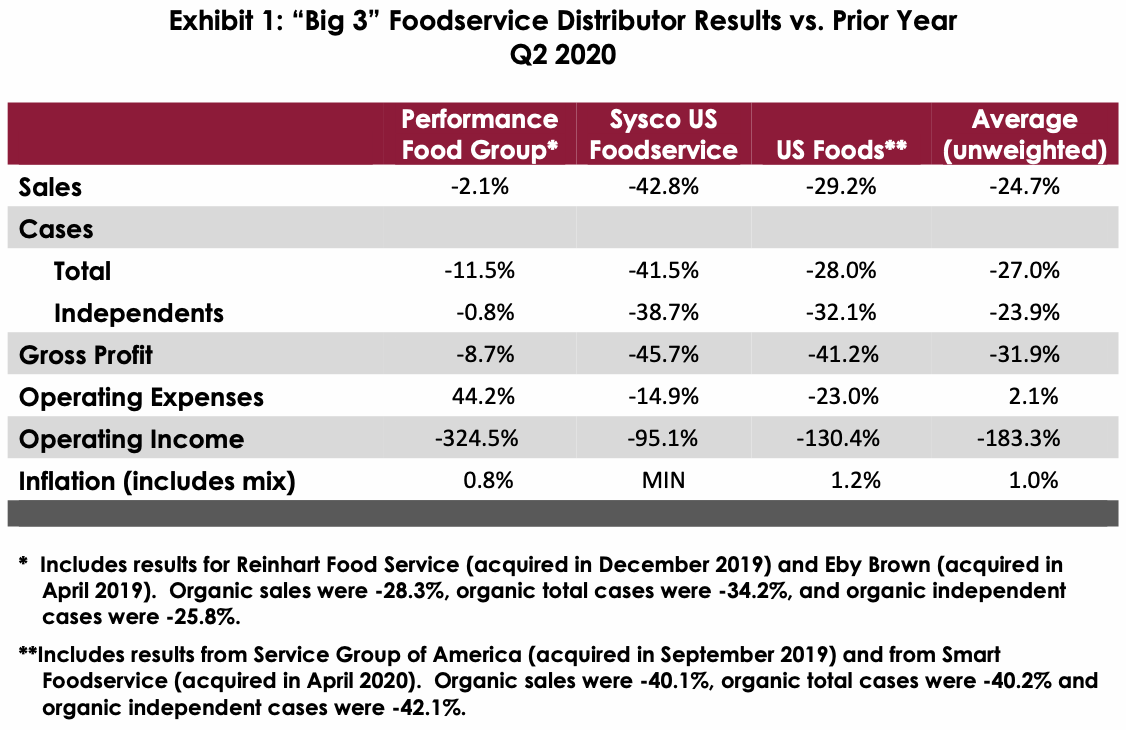

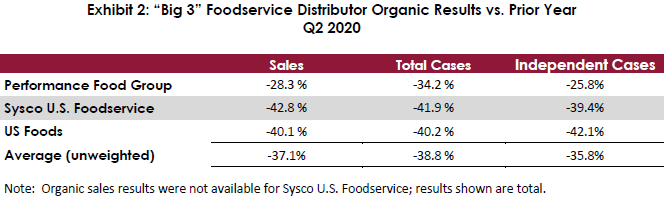

The latest quarterly results from the Big 3 foodservice distributors (Performance Food Group, Sysco and US Foods) provide ample evidence of the hugely adverse impact the Covid-19 pandemic is having on the foodservice industry. All three companies suffered significant declines in volume and profitability and lost money during the second quarter of this year¹; as shown in Exhibit 2, their organic sales and case volume trends are a clear indicator of dismal industry conditions during the April – June period, during part (or all) of which time most markets were under voluntary or mandated closures and/or severe access and operating restrictions.

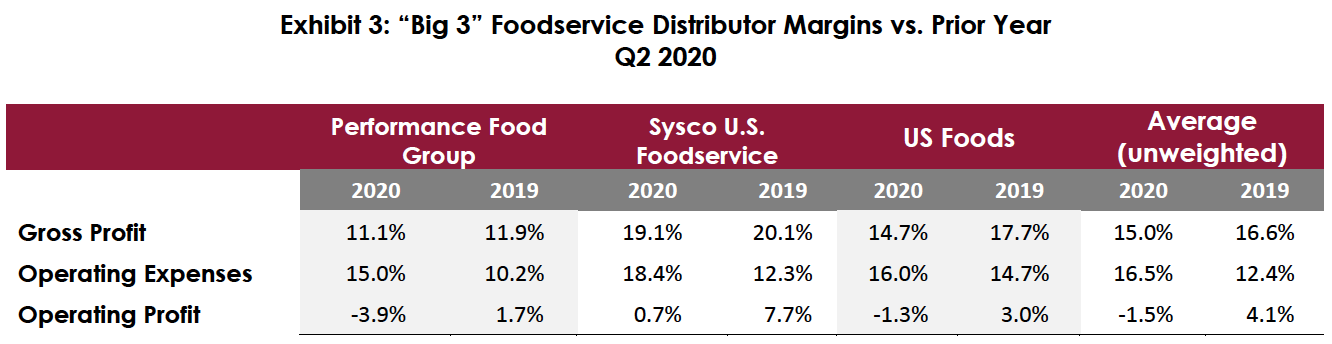

To their credit, the Big 3 acted aggressively and rapidly to enhance their balance sheets, improve working capital management, reduce their fixed and variable cost structure, pursue profitable new business, diversify their revenue streams and support their key customers. Despite a cratered economy, massive uncertainty, deteriorating margins (as illustrated in Exhibit 3) and diminished near and intermediate-term prospects for some of their businesses, the companies now have much greater liquidity and structurally lower expenses which will likely enable them to gain market share for the foreseeable future.

A few additional comments and observations relative to market conditions and distributor performance:

- Chef’s Warehouse is a publicly traded foodservice distributor specializing in higher end independent restaurants in major metro markets. As such, they are a good indicator of segment performance. During the second quarter, their organic sales were -57.8%.

- Sysco’s chain specialized division, Sygma, had previously been a laggard in the portfolio due in part to a very challenging pre-pandemic labor market. Last quarter, Sygma greatly outperformed the U.S. Foodservice (broadline) division; its sales, gross profit and operating profit were -16.8%, -11.2% and -13.4%, respectively. As reported in Exhibit 1, the comparable figures for Sysco U.S. Foodservice were -42.8%, -45.7% and -95.1%.

- Performance Food Group’s Vistar division had been the company’s major growth driver; it is now underperforming the other divisions due largely to its customer mix (theaters, OCS, mini-markets, etc.).

- While there is some inconsistency in how the major contractors (Aramark, Compass and Sodexo) classify segments and measure results, they are reporting steep declines, reflective of the challenges most institutional segments are facing. For the most recent reporting period, Aramark’s U.S. revenues were -56%, Compass’ were -45% and Sodexo’s were -37.3%².

- Independent restaurants are a major user of distributor branded products. Given the sharp decline in that segment, distributors will be challenged to meet their brand development objectives, which may impede their margin growth.

During analyst presentations, senior management of the referenced companies cited a sequential (albeit spotty) improvement during the quarter, a belief that they are doing relatively better than the industry as a whole, and some level of optimism about the industry’s near-term recovery prospects. While Pentallect recognizes the long-term growth potential of foodservice, we expect the industry rebound will be very protracted, with a return to overall pre-Covid levels unlikely prior to 2024. Further, we believe that a number of segments, most notably travel and leisure, will be permanently impaired. And, unfortunately, we anticipate that operator closures and distributor failures will accelerate over the next several months, absent additional and substantial government relief.

¹ Sysco U.S. Foodservice made $41 million; the parent company lost $531 million.

² Revenues for Compass and Sodexo were for North America.