Despite industry-wide restaurant traffic declines, some trading down and ongoing (but moderating) cost pressures, the “Big 3” foodservice distributors’ third calendar quarter results for 2022 met or exceeded analyst expectations for sales and profitability and indicate market share and customer penetration (“share of wallet”) gains. These favorable results clearly reflect the companies’ prudent strategic focus on and effective execution of value-driving initiatives such as inbound freight optimization, customer and product mix improvements, customer and channel diversification (including acquisitions) and investments in human resources and technology. Perhaps most tellingly, the results reflect a resilient end-market that has, to date, generally accepted painful menu price increases. As a sure sign of optimism, the companies are in the process of or have announced plans to reduce leverage, increase dividends1, repurchase shares and/or raised future guidance.

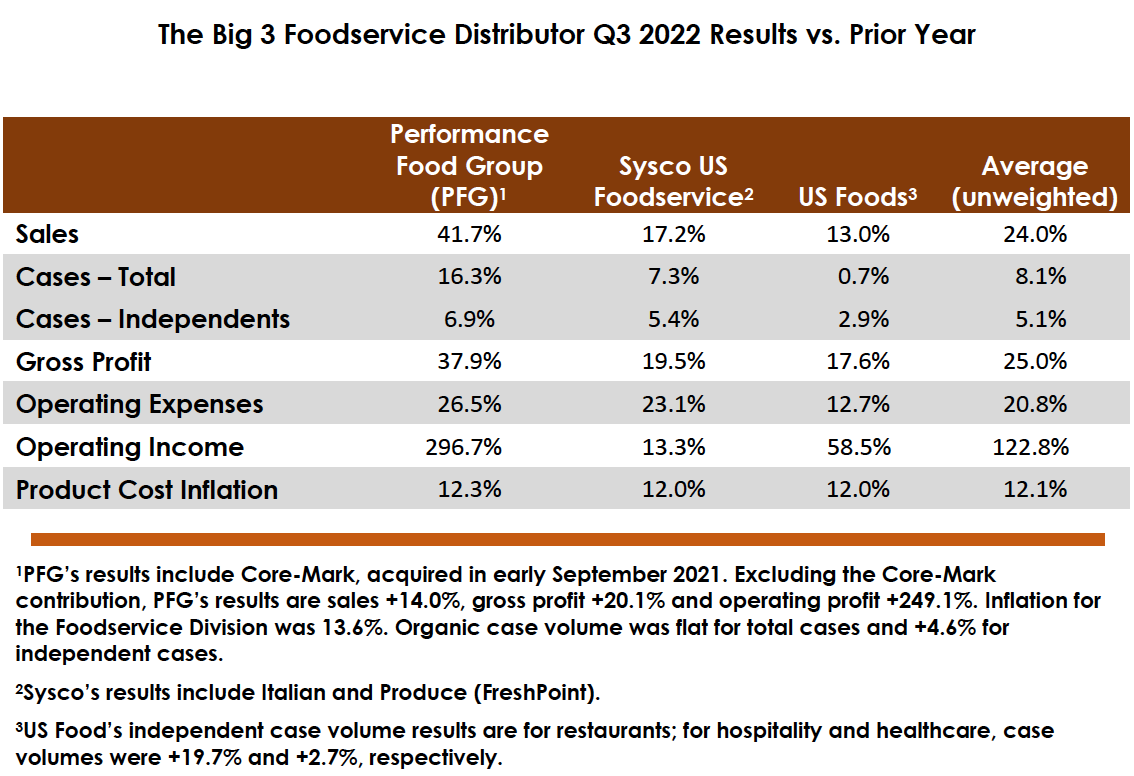

As shown below, the “Big 3” had an unweighted average increase of 24.0% in sales, 8.1% in total case volume (2.7% on an organic basis) and 25.0% in gross profit; excluding PFG’s Convenience and Vistar’s Division, “Big 3” sales were up 15.1%, which is “above market”. Operating expenses were up 20.8% due in part to the high costs of “overservicing” customers and problem resolution; even with inflation, this expense growth is not sustainable over an extended time. The other major publicly traded foodservice distributor, The Chefs’ Warehouse (a $2+ billion distributor of specialty food and center-of-the-plate items to fine dining establishments and independent restaurants) grew sales and gross profit by 36.3% and 43.5%, respectively, on organic increases of 18.3% for specialty food cases and 11.6% center-of-the-plate pounds.

Significantly, the reported results show an impressive increase in gross profit per case, a key performance indicator, and a sequential deceleration of operating expense increase. These factors will lead to ongoing earnings leverage, which we expect to be significant over the next several years.

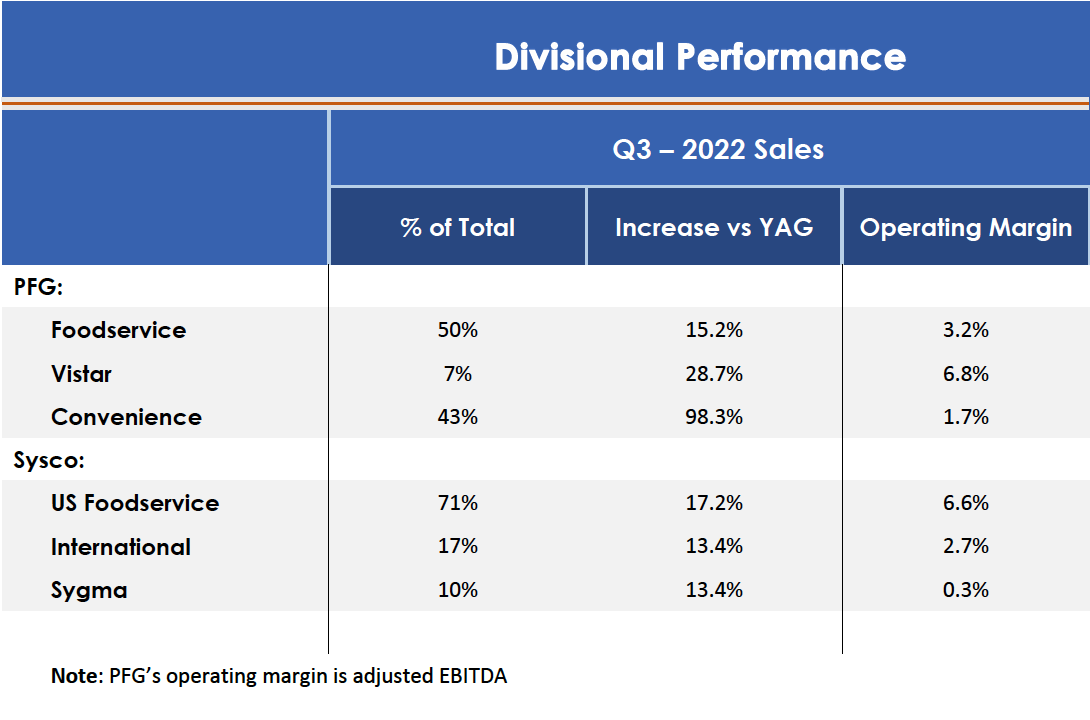

PFG and Sysco report divisional performance. For both companies, the foodservice (primarily broadline) division is the most profitable and is showing solid organic growth. US Foods just announced plans to open six additional Chef’Stores this year so we assume the division is meeting company expectations.

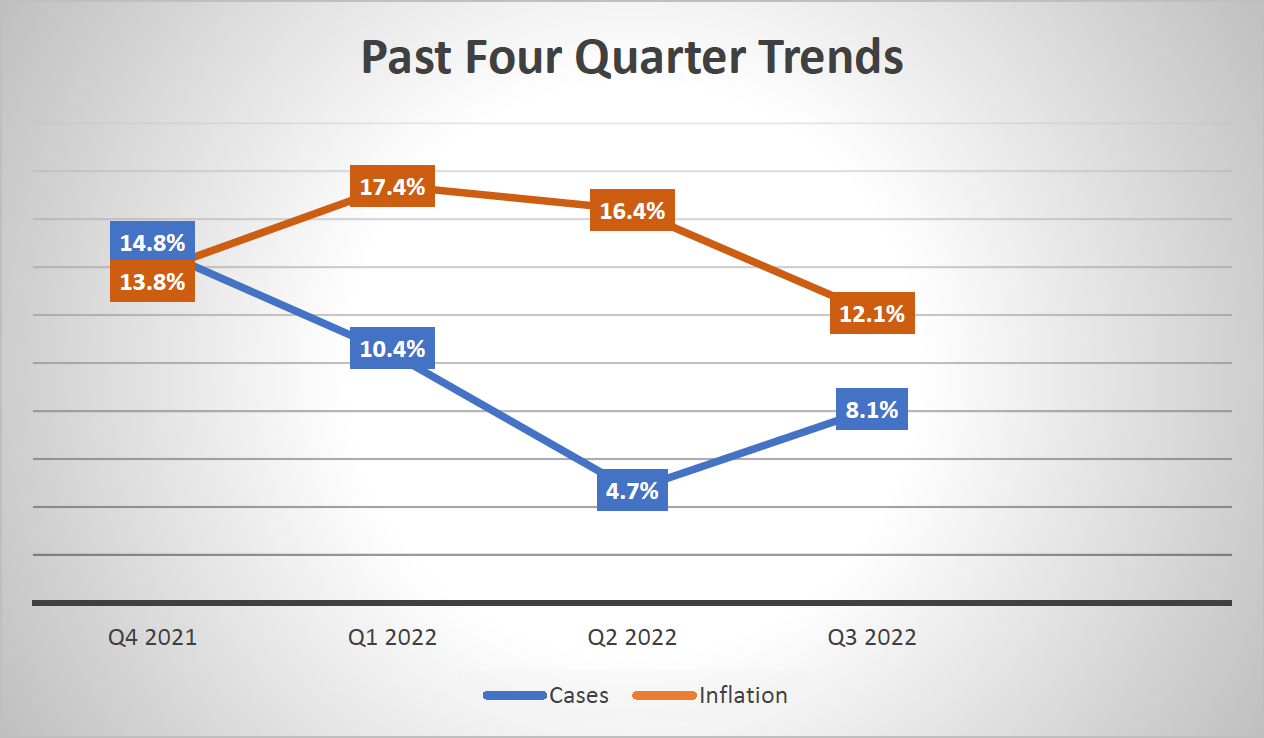

Based on remarks by the distributor senior management, published data and our observations, it does appear that product cost inflation is easing in many categories such as proteins, the labor situation is improving (although problems with labor unions are more common), inbound fill rates, while still problematic, are on the upswing and customer receptivity to distributor brands is increasing in this environment. We do expect the “Big 3” and other major distributors to diversify their supplier bases to improve supply chain reliability.

As in other challenging macro-economic times, the foodservice industry has once again proven to be on a long-term secular growth pattern due to its alignment with key consumer demands. This alignment has provided trade the ability to pass along cost increases with fairly limited consumer “pushback”. The “Big 3” have made appropriate course corrections and are in an enviable position to benefit considerably from a normalizing market.

1Sysco announced a dividend increase earlier in the year. It is a “Dividend King” – a company that has increased dividends annually for the past 50 years. There are currently 48 “Dividend Kings”.

By: Bob Goldin, Barry Friends and Chris Davis

For additional insights, please:

Contact Us