![]()

By: Bob Goldin | Barry Friends

November 8, 2020

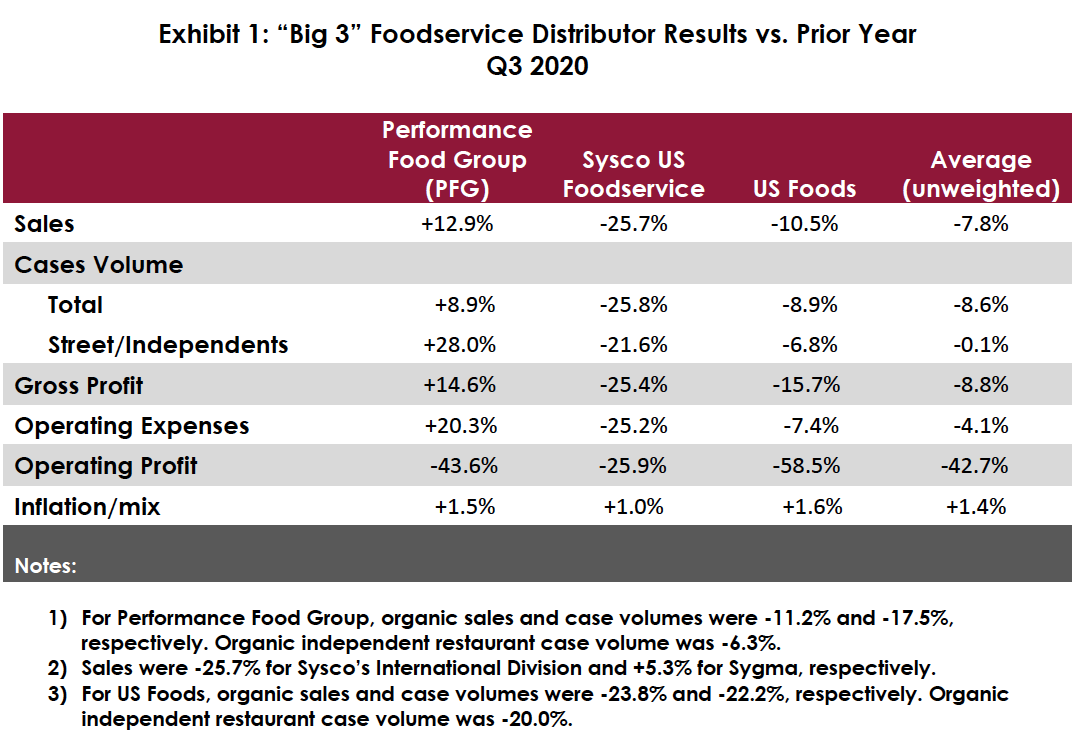

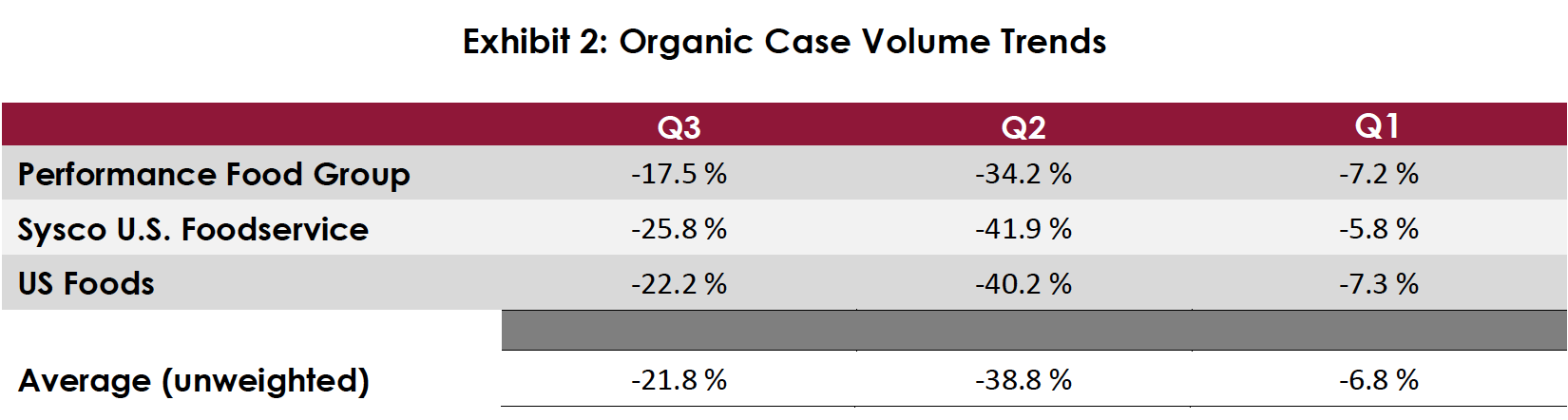

On the heels of a brutal, pandemic-induced second quarter that resulted in an average organic case volume decline of 38.8%, the “Big 3” foodservice distributors reported improved results for the most recent quarter (July – September). Tellingly, the remarks made by the companies’ CEOs during earnings calls indicate general optimism about a relative near-term industry recovery, market share gains and new business wins, and bullishness about their future prospects. The referenced companies have clearly done a masterful job in leveraging their scale, making structural cost reductions, improving their customer mix, accelerating their digital initiatives, generating cash flow, and bolstering their liquidity (PFG reports having around $2 billion in liquidity, Sysco $8 billion and US Foods $3 billion). As shown in Exhibit 1, despite the reduction in operating expenses (by Sysco US Foodservice and US Foods), sharp case volume declines (averaging 21.8% per Exhibit 2) continue to cause reductions in gross and operating profit. Note, however, that Sysco and US Foods both generated positive cash flow this quarter.

The “Big 3” each have a large and diverse customer base that is reflective of the overall market, exclusive of major quick service restaurant chains that are serviced by custom distributors. As such, their (organic) case volume trends are a reliable indicator of broad market trends. However, each distributor contends that their customers tend to “outperform” the average; if that is indeed the case – and we believe it likely is – the foodservice industry was down in excess of 21.8% (more likely in the 25 – 30% range). The Chef’s Warehouse, the other publicly traded foodservice distributor, focuses on higher-end full-service independent restaurants in major metro markets. It reported case volume declines of 49.3% for their grocery (specialty) lines and 45.4% for center-of-the-plate, representative of the much poorer-performing “dine-in” segments suffering from capacity constraints and (valid) consumer safety concerns

Among the “Big 3,” PFG is somewhat less exposed to the most negatively impacted major urban markets than US Foods and Sysco, especially with the recent addition of Reinhart’s many secondary and tertiary market locations. Coupled with their Roma Foods legacy strength in the independent pizza/Italian segment, PFG has suffered slightly less “damage” than their other two peers, although their Vistar Division has been severely disrupted.

Some or all of “Big 3” made several comments of note:

-

- Restaurant closure rates are lower than expected. We note that there is conflicting external data on closures. We further note that it is not possible to distinguish between temporary vs. permanent closures.

- Major urban markets are struggling far more than suburban and smaller markets due to various shut-downs and restrictions, huge decreases in business travel and tourism, and the like.

- The competitive environment is “rational.”

- Many operators, including chains, are seeking secure supply sources, which favors companies like the “Big 3” and translates into profitable new business opportunities.

- Collection efforts have been successful for the most part and enabled favorable adjustments to bad debt reserves.

- Vendor service levels continue to be a challenge; in response, distributors are increasing their inventory levels.

- Major opportunities exist to capture a greater share of independent customers’ “wallet” (Sysco estimates that the industry average for the primary distributor is in the 30% range, which dovetails with Pentallect data).

- There is strong and growing evidence of pent-up demand for food away-from-home (and corresponding fatigue with food at-home) which will speed up the industry’s post-pandemic recovery.

We truly commend the prudent and effective management and, under the circumstances, solid results of the “Big 3.” The companies have clearly demonstrated strong leadership, adaptability and strength in terribly trying times. However, we are deeply concerned about the duration and severity of the pandemic and how it will continue to adversely affect foodservice and the overall economy here and abroad. New restrictions in many large markets coupled with colder weather and lack of government relief will present headwinds that will pressure all foodservice value chain participants. While we have no doubt that the “Big 3” have improved their competitive position and are “doing the right things”, we expect them to struggle along with others in our industry.

¹ Note that the case volume trends include new customers and greater penetration of existing accounts

² Sysco’s Sygma Division is a custom distributor; its results are not included in Sysco US Foodservice data presented