{kind=link}

By: Bob Goldin | Barry Friends and Bob Planck*

November 14, 2019

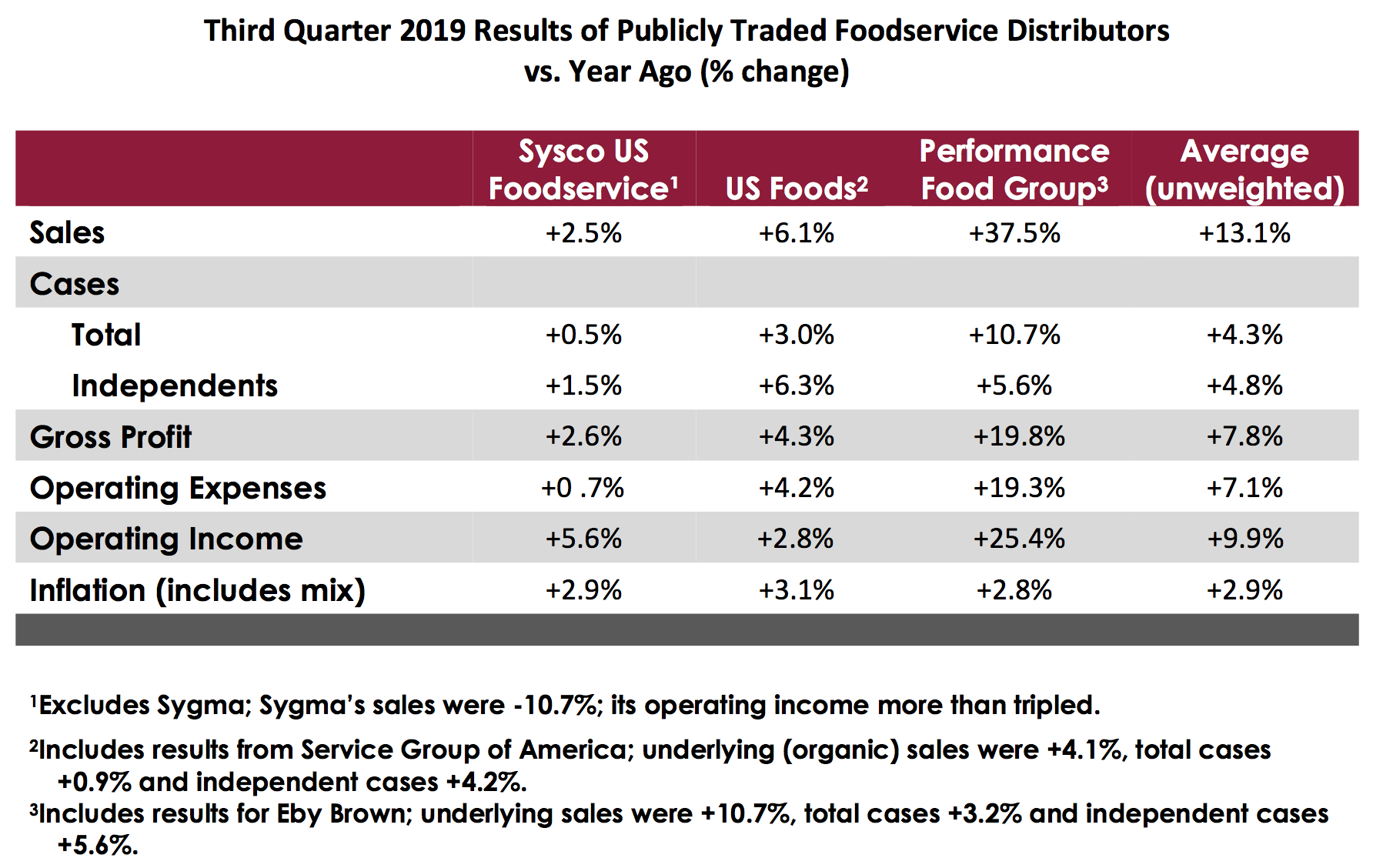

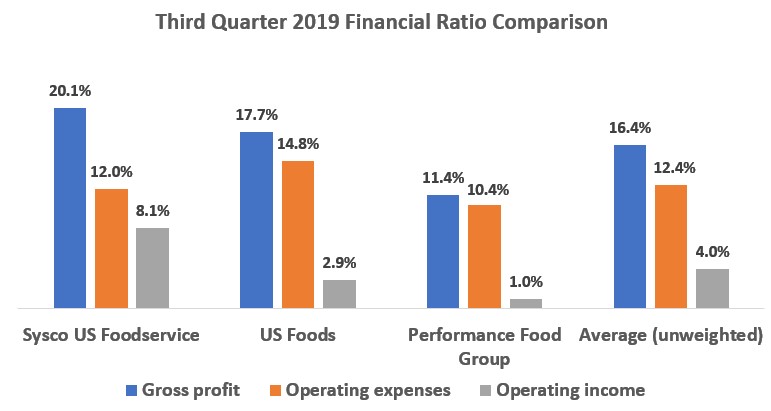

The latest quarterly results of the “Big 3” publicly traded foodservice distributors – Sysco, US Foods, and Performance Food Group – reflect very solid performance on all key metrics, most notably improved profitability (all three companies achieved increases in gross profit per case, a major operating profit determinant). For the most recent quarter, these three companies had almost $25 billion in combined domestic sales and $1.1 billion in operating income.

To varying degrees and against some challenging industry conditions (including very serious labor shortages in many markets), the referenced companies are benefitting from strong continued growth in their high margin “independent” businesses (where they are gaining valuable share), success in building their exclusive brands (primarily at the expense of manufacturer brands), effective customer targeting and development, strategic investments and operating expense control. Sysco is doing a particularly impressive job with operating expense control, giving the company huge earnings leverage and setting ever-higher benchmarks for the industry at large.

US Foods and Performance Food Group volumes are being favorably and significantly impacted by their recently completed acquisitions; conversely, Sysco’s overall business is being adversely impacted by revenue and profit declines in its International Division. Going forward, the acquired companies (including Performance Food Group’s pending acquisition of Reinhart Food Service which is expected to be completed later this year or early 2020) will play an even larger accretive role in their parent companies’ results and overall capabilities.

The foodservice distribution industry is concentrated – Pentallect estimates the “Big 3” currently have a 33% share of the market – and consolidating at a fairly rapid rate. The major broadliners have amassed significant scale that they are leveraging to service the needs of their target customer bases, lower their cost structures, expand their networks and further increase their “clout” with suppliers. We fully expect them to continue to “double down” on these strategies that have enabled them to achieve such impressive results, including even more aggressive operating expense control.

One of their core strategies has been customer mix improvement, which has led to an overall reduced focus (or, perhaps better stated, far more selectivity) on chain restaurant customers. This has predictably caused some concern among some chain customers and may result in an enhanced opportunity for chain-oriented distributors and co-ops like DMA.

Sysco, US Foods and Performance Food Group all trade at above market PE ratios**, a sign that the “market” respects and rewards the companies’ excellent and consistent performance and likely perceives them to have untapped potential. While Pentallect projects the foodservice industry to grow sluggishly in 2020, we fully expect the “Big 3” to outperform their competition by a widening margin.

**As of the date of this article, the average PE ratio of the Dow Jones Industrial Average is 20.6; Sysco’s PE ratio is 24.5, US Foods’ is 21.6 and Performance Food Group’s is 26.9

* Bob Planck, a valued Pentallect affiliate, is the founder and former CEO of Independent Marketing Alliance (IMA)